Digital disruption in Consumer Goods business and e-commerce development in the Baltics

Tallinn, Estonia – Kairi Raudmets, Country Manager for Estonia, interviewed two top representatives of the global Fast Moving Consumer Goods companies in the Baltics: Arturs Kanepe, Reckitt Benckiser Country Manager Baltics and Aleksandr Ugorenko, former Baltic Countries Director at Unilever.

Over the past few years, e-commerce has become a significant part of the corporate agenda for FMCG companies in the Baltics. There are plenty of successful global examples – Amazon, Alibaba and eBay have been disrupting the retail sector for many years and show no signs of stopping – where consumers have benefited from the speed and convenience of purchasing, while companies have gained from increased revenues.

It is therefore not surprising that FMCG companies in the Baltics are also jumping on the bandwagon and considering various ways of blending technology into their operations. Moreover, the three Baltic states have all the necessary prerequisites for the successful implementation of technological developments, such as:

- Technological advancement; for example, Estonia ranks 9th in the EU's Digital Economy and Society Index (DESI) 2017

- EU and Eurozone membership

- High internet penetration and speed

- Active and well-established startup ecosystem

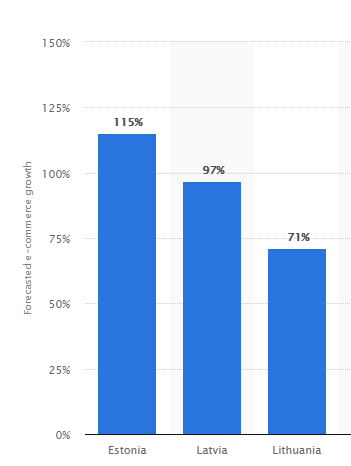

Projected e-commerce growth in the Baltics 2015-2020. Source: Statista.com

Of course, there are challenges. One of them is market size: all three countries are relatively small, and although they are usually grouped together, there are differences between them – the most obvious one being language. Scalability is a challenge with these small markets, where campaigns and communications must be adapted to three different languages.

I interviewed two very successful representatives of global FMCG companies in the Baltics, and discussed the road to success and barriers in the e-commerce development in the Baltics. We also review what digital disruption means for a small market, and how it can happen.

1. How do you see your company’s global e-commerce strategy in the Baltic context here and now, and what could the future look like?

Aleksandr: We are definitely moving toward introducing e-commerce, but these are still baby steps in the Baltics. Estonia is a bit more advanced, yet lags behind the big markets like the US or China.

Arturs: Even Poland, while still very small in terms of the total volume of business, is more advanced than the Baltics, which is expected.

Despite this, the e-commerce penetration could grow tenfold if activated and strategically focused.

2. What changes do you see in the digital world, and to what extent will it change your product marketing and sales channels strategy?

Arturs stated that in every market, his company must start to develop online sales channels from scratch, as they don’t have their own online platform (and do not plan one in the nearest future).

In Poland, for example, digital sales are growing as a proportion of total sales, so it’s important to conduct research to find out how the product is bought, through which channels, and who influences the online decision-making before jumping into the implementation phase.

Regarding marketing channels, TV is still by far the most effective way to attract the consumer. Other channels such as YouTube, Facebook, blogs, Instagram, and other social media are becoming more effective in terms of brand building and helping create awareness of the products, but the bulk of the advertising budget still goes to TV. At the same time, the shift of marketing budgets from TV to other channels has caused an increase in the cost of GRP (gross rating point measuring the impact of advertising), meaning that the less TV time you buy, the higher the unit price. At the same time, online media channels also require investment, which at this time does not produce the necessary impact.

In terms of sales channels, as mentioned above, global consumer goods companies use established online retail channels and do not have their own platforms. In the Baltics, the most successful so far are Maxima at the pan-Baltic level, and Selver in Estonia. Drogas is also becoming a strong player. The other online stores are still so small in terms of size and volume that the focus on them is not justified.

Another important factor to keep in mind is supply. In small markets, not many companies have the capacity or logistics to make a full range of goods available to customers when they want them and where they want them. However, the consumers in the Baltics do not understand why they can’t buy the same products online as anywhere else in the world.

Consumers expect to have a product no later than the next day, especially a basic everyday product. They are not prepared to wait from five days to two weeks for a global company to deliver it to them. At the same time, the big players like Alibaba, E-buy, and Amazon have no interest in entering small markets like the Baltics. The challenge to be solved is the logistics of getting the product from the factory to the consumer.

Additionally, the complexity of delivery and returns must be solved at a local level, and this is not cheap. All processes starting from product delivery, pricing, returns, etc. need to be aligned and agreed. In this sense, establishing an online business is similar to setting up collaboration with a new physical retailer. The small-scale Baltic markets make this exercise expensive for everybody, although the consumer wants to buy a product at the same price as a physical store. Consumers expect to be able to order products with one click, and for the search engine to automatically find the closest service provider. This is the future, but the road ahead is long.

Investing in multiple channels has put pressure on consumer goods companies in the Baltics, and is hitting their bottom line. Retailers expect the manufacturers to maintain their investments in stores by providing gondola ends, displays etc., as well as in online retail. Therefore, new agreements must be negotiated to balance the investments. A good partnership with the retailers is the key to finding common solutions for attracting and satisfying consumers.

3. How does consumer shopping behavior differ for online vs physical stores, and what impact do they have on each other?

Aleksandr and Arturs agreed that while books and electronics product groups are more likely to be bought online as one can check all the features of an electronic device without physically touching it, food and general consumer goods are different.

People are conservative in buying generic consumer goods, and still prefer to touch them to ensure they are getting exactly what they want. While the final shopping decision still happens inside a store in many cases, we see an increasing number of people making their general selection online, and then going to a physical store to make the purchase. Ideally it should be a symbiotic situation, as the online and offline channels address different needs and concerns of the consumers.

One such concern is trust in buying online. Although one person in five could potentially make purchases online, consumer habits in the Baltics are not yet ready for mass e-commerce (except for Maxima and Selver, mentioned earlier). Still, online purchases constitute a very minimal share of the total basket of goods.

4. Will consumer goods companies be able to offer a serious competition to retailers in the future with their own online stores? How will digital disruption change the retailers?

Currently, no one knows how things will eventually develop. Some markets are more advanced, and are moving towards consumer convenience. Retail stores will need to be more entertaining than they used to be, and the retailers must work harder to keep up with changes.

As for the future, it looks promising. While FMCG e-commerce in the Baltics is still taking baby steps, it’s growing rapidly, and in many cases, we see online and offline retail seamlessly complementing each other. For example, consumers need the familiarity and entertainment of bricks and mortar shops, as well as the touch and feel of the real products, but want to gather information and compare prices online first.

Following this interview with Arturs and Alexandr, as well as my own observations of market trends, what we can say with confidence is that the current retail sector will go through significant changes in the future. There are already some innovators out there who know how to make the online customer experience as safe, trustworthy and welcoming as one might expect from a reputable branded physical store. Thanks to smart contracts, once businesses have built their online reputation, there will be no need to start again and again when entering new online channels.

Furthermore, blockchain is bringing us to the internet 2.0 stage, which will help us to simplify and expand human agreements (smart contracts). Blockchain will disrupt all businesses globally, and most specifically in the retail sector, helping. them to become part of a full ecosystem where a consumer will be able to see the full cycle of a product and find out, for example, whether coffee was sourced from a fair-trade producer, or a wine has been shipped to them at the agreed temperature. There will be wallet refrigerators that can automatically order food and instantly transfer payment. And if your favourite wine is out of stock, your wine cooler will automatically send the order to your supplier and request instant delivery.

As everything will be connected, groups of companies will be able to provide discounts on purchases that are done within the same ecosystem. This will benefit the retailer in terms of extra sales, and the consumers who will be receiving targeted offers in which they are actually interested.

Additionally, clients will be able to track how long a product has been in the warehouse, which will improve the quality of service and experience for both the manufacturer and consumer. Food products will be tagged so that consumers can be sure of their sources and origins. And this is just the beginning.

In conclusion, FMCG and retail companies should both remember that the ultimate driving force behind the changes are customers. Businesses need to listen to them and to create personalised convenience. Leading markets in the digital age will come from having the right data, and the right people with the capabilities to analyse and apply it in a meaningful way that anticipates and meets consumer needs.

Kairi Raudmets is the Country Manager for Estonia at Pedersen & Partners. Ms. Raudmets brings to the firm more than two decades of in-depth functional sales and marketing expertise in the FMCG and Travel & Leisure industries. Prior to joining Pedersen & Partners, Ms. Raudmets spent 11 years with global food products manufacturer Mars – creating, recruiting, leading, and developing multicultural and often remote sales and marketing teams in the Baltics. She managed business in Estonia, drove customer and category management in the Baltics and contributed to the regional business growth as a member of the leadership team. Ms. Raudmets started as a Key Account Manager, was promoted to Country Sales Manager for Estonia and eventually became the Customer Marketing Manager for the Baltics. Her professional career began in the Travel & Leisure industry, where she held roles with travel services providers and an international hotel chain.

Kairi Raudmets is the Country Manager for Estonia at Pedersen & Partners. Ms. Raudmets brings to the firm more than two decades of in-depth functional sales and marketing expertise in the FMCG and Travel & Leisure industries. Prior to joining Pedersen & Partners, Ms. Raudmets spent 11 years with global food products manufacturer Mars – creating, recruiting, leading, and developing multicultural and often remote sales and marketing teams in the Baltics. She managed business in Estonia, drove customer and category management in the Baltics and contributed to the regional business growth as a member of the leadership team. Ms. Raudmets started as a Key Account Manager, was promoted to Country Sales Manager for Estonia and eventually became the Customer Marketing Manager for the Baltics. Her professional career began in the Travel & Leisure industry, where she held roles with travel services providers and an international hotel chain.

Pedersen & Partners is a leading international Executive Search firm. We operate 56 wholly owned offices in 52 countries across Europe, the Middle East, Africa, Asia & the Americas. Our values Trust, Relationship and Professionalism apply to our interaction with clients as well as executives.

If you would like to conduct an interview with a representative of Pedersen & Partners, or have other media-related requests, please contact: Anastasia Alpaticova, Marketing and Communications Manager at: anastasia.alpaticova@pedersenandpartners.com